Money Management for Neurodivergents

‘‘Part 1: Meet Your Money Goals’’

Author: Chris Kinion

Date: April 2, 2026

Disclaimer: "I am not a licensed financial advisor. The information on this site is for educational purposes only and should not be considered personal financial advice. All investments involve risk, and all decisions are made at your own risk".

Part 1: Meet Your Money Goals

Part 2: Budget to Meet Your Goals

Part 3: Save to Meet Your Goals

Part 4: Invest to Meet Your Goals

Part 5: Protect Yourself to Meet Your Goals

Marriages can survive a lot of things. But they require two people committed to working in the same direction for the same reasons. Disagreements on money - often an indication of other problems - frequently precedes divorce.

My divorce was no exception.

As an undiagnosed autistic adult, I struggled with impulsive spending and racked up a lot of debt. So did my wife. When we finally decided to communicate with one-another about needing to get out of debt, it was too late. We lost almost everything before finally separating.

Years later, I remarried. Despite my hard work and determined saving, I lost my job. I went back to school and ran out of money before graduating and getting my first analyst job. I was better prepared, but it was one of the hardest experiences of my life.

Losing a source of income is not unique to neurodivergents, but it affects us deeper and longer. Everyone will experience some financial hardship. In this series, I will share my experiences and help you develop a better relationship with money.

I struggled with money for years for four reasons:

I didn’t have a good plan

I didn’t save enough

I didn’t invest wisely

I trusted the wrong people

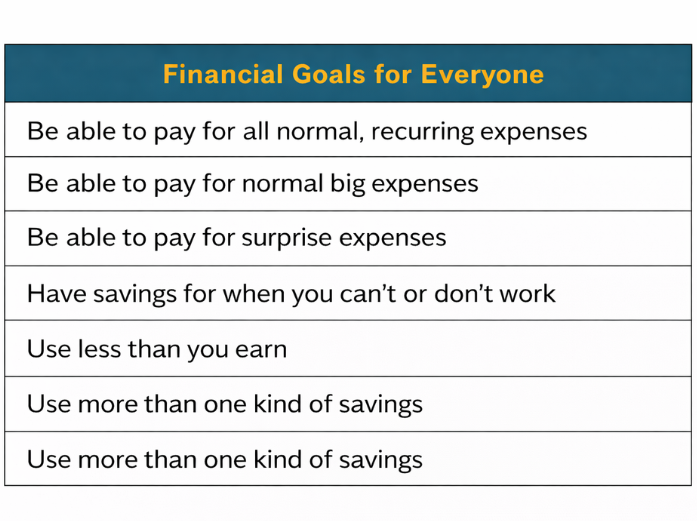

Unless you address these obstacles, you will fail to meet your money goals. In no particular order, your goals should include the following:

Once you’ve had time to actually meet and exceed these goals, you can do some really interesting things with your time and money. But if you are not financially literate, how can you expect to make good financial decisions?

My first wife and I had very little financial education. We knew we were supposed to have a budget, so we split our expenses between the two of us. Beyond that, our money was our individual responsibility.

We failed to consider that we would need to take care of unplanned expenses. We didn’t work towards any kind of savings goals. We didn’t communicate about important things - like our personal finances - so we weren’t effective partners for each other.

Towards the end of our relationship, some friends introduced us to Dave Ramsey’s “Financial Peace University”. We made progress, but trusting the wrong financial advisor wrecked our finances. Eventually, our money problems became a metaphor for our relationship: we were ready to give up.

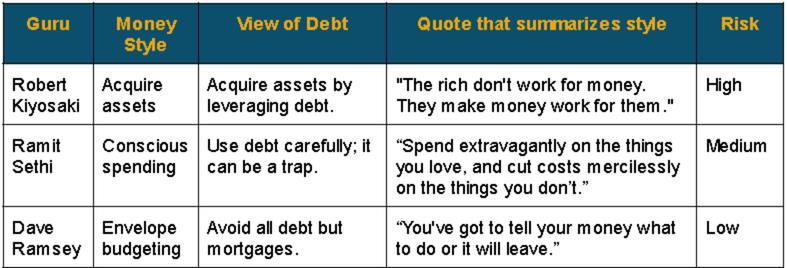

Several financial “gurus” embody the different styles of managing money, though none of the techniques are owned by any one person. Rather, they market their methods well enough that sometimes it’s easier to describe the style by the guru.

Ultimately, you have to decide for yourself what works best for you by taking the best of each style and making it your own.

Here’s a quick breakdown of the most representative financial gurus and their styles:

I do not endorse or get paid by any of these people. I favor the Sethi and Ramsey methods for neurodivergents and young adults, though ultra-wealthy NDs like Elon Musk operate exclusively by Kiyosaki’s principles. Unless you’re a successful entrepreneur, Kiyosaki’s methods won’t apply to you; if they did, you probably don’t need his advice.

Before I continue with the series, I recommend the following two books to anyone wanting to improve their financial literacy:

Complete Guide to Money, Dave Ramsey

I Will Teach You to be Rich, Ramit Sethi

These two books cover 99.5% of everything most people will ever need to know about money, budgeting and investing plus a reasonable amount of each author’s personal take on finances. If I could only gift one from the used book store, I would pick Sethi’s every time: It covers every aspect of banking, budgeting and investing that I wish I knew 25 years ago.

Next in the series, “Budget to Meet Your Goals” I will talk about some neurodivergent-friendly ways to manage your money in order to meet your needs and prepare for emergencies.