Budget to Meet Your Goals

“Part 2 of the Money Management for Neurodiverts Series”

Author: Chris Kinion

Date: April 16, 2026

Disclaimer: "I am not a licensed financial advisor. The information on this site is for educational purposes only and should not be considered personal financial advice. All investments involve risk, and all decisions are made at your own risk."

Part 2: Budget to Meet Your Goals

Part 3: Save to Meet Your Goals

Part 4: Invest to Meet Your Goals

Part 5: Protect Yourself to Meet Your Goals

Never wonder where your money went again. Follow along as we build a friendly budget for neurodivergent brains.

Sarah is our imaginary AuDHD (autistic, ADHD) young adult who has a job, lives on her own, and needs to prepare financially for life. She loves coffee with friends and having her nails done at the salon. She also feels embarrassed because she never seems to have enough money when bills are due.

Over her lifetime, Sarah may be unemployed longer and more frequently than her peers. She also struggles with impulsive spending and demand avoidance, which sometimes makes the difference between doing what she needs to do and what she wants to do feel insurmountable.

Sarah needs a plan for her money: a budget.

“Budgeting is telling your money where to go instead of wondering where it went.”

Like many autistic and ADHD adults, just thinking of creating a budget spikes her anxiety. To sit down and focus on this task feels like an impossible challenge. Let’s help Sarah with her financial hygiene - the health of her finances - so she can live independently and prepared for the future. We will use automation to reduce her anxiety and make sure her bills get paid on time. We will also give her a way to spend on the things she wants and still prepare for the future.

Banking Requirements

My recommendations for Sarah are largely inspired by Ramit Sethi’s principles. She will have a total of three checking accounts and one savings account at an online bank that does not charge her or require a minimum balance. She will use one of Ramit Sethi’s recommended banks.

She will automate her money by depositing all her income into a primary checking account. Once she figures out her budget, she will use automated withdrawals and transfers to fund all her other activities.

After she builds a small balance in the primary checking account, she attaches automatic payments for her rent and other recurring expenses to it. For her regular expenses like food and gas that vary in size and frequency, she sets up an automatic transfer from the primary account to a variable expense account. She then sets up an automatic transfer from the primary account to the last checking account for no guiltspending account. Lastly, she sets up automatic transfers to her savings account which she will use for very specific situations.

If Sarah needs cash for her no guilt spending, she can use her debit card at almost any ATM. Her bank will refund up to a certain amount of ATM fees, saving her money. She can also use the bank’s phone app to monitor all her accounts so she knows how well her plan is working and can plan accordingly.

I emphasized the “no guilt” account for Sarah because it helped my spouse finally get on a budget. By funding a “no guilt” account, she chooses when and how much to spend, not a spouse or budget. Spend it on coffee? No guilt. Save for a new gaming system? No guilt. Travel? No guilt! It allows you to spend lavishly on the things you love and stay within your means.

“Spend extravagantly on the things you love, and cut costs mercilessly on the things you don’t.”

Making an Automated Budget

To help Sarah get started, I asked her to provide:

Her spending records for the past 3 months

Her bank information

A spreadsheet like Google Sheets (a free online tool)

Preparing and living a budget always follows the same pattern:

List your income.

List and categorize your expenses.

Matching your money to your goals (making the budget).

Spend according to plan.

List your income

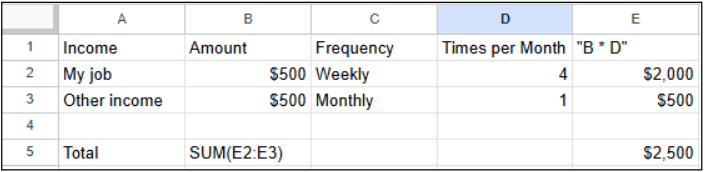

The easiest part of the budget process is to determine income. How do you get paid? How often do you get paid? How much do you get paid? I had Sarah write down what she gets paid after deductions.

Note: The pictures show formulas, but to actually use them you’ll need to type the equal sign = before the formula. For example:

=SUM(E2:E3)Here, Sarah gets paid $500 each week plus gets an additional $500 each month from an additional source of income for a total of $2500.

2. List and categorize your expenses

The hardest part of budgeting is to honestly examine your expenses. If you use a credit card or debit card, this will involve looking at your bank statements. If you use cash, you will have to spend some time tracking how that cash is spent. But understanding how you spend is less a judgement and more a data point for this step.

I had Sarah categorize each transaction into three categories: No Guilt, Necessary and/or Recurring, Necessary and Variable. These correspond directly to the three checking accounts I had her set up!

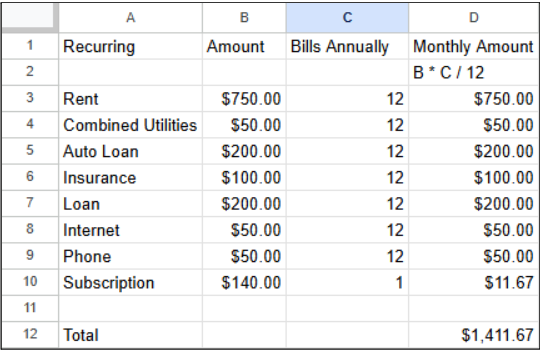

Necessary and/or Recurring: This category includes any recurring expense that is the same from month-to-month. It includes rent, subscriptions, insurance, loans and sometimes utilities.

Notice that Sarah has an Amazon Prime membership that charges once per year, so we calculated its average monthly cost.

Note:

Viewing your budget a month at a time is the most convenient way to manage your money. Few lenders bill more than once per month, while some subscriptions bill once per year. Calculate the average monthly cost for that expense and figure that into your budget by finding the cost for the expense for an entire year and divide by 12.

She will set all of these payments to automatically draft from her primary account. She’ll never be late on a payment again!

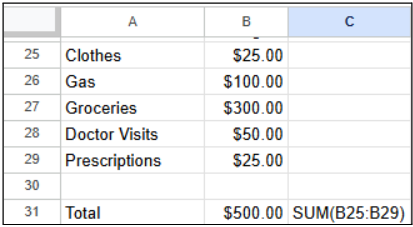

Necessary and Variable: This category includes any regular expense that doesn’t have a set value like transportation, clothing and food expenses. Your expenses will likely be different from Sarah’s.

To get started, we just need to know what we currently spend, so an average over three months will get us pretty close.

No Guilt: This category includes anything else that does not fit into the other categories. If Sarah never put any money in this account, she could still pay for all her living expenses with the other two. Generally, I recommend putting dining out, hobbies and entertainment in this category.

Sarah likes decorating her nails and drinking coffee. So long as there’s money in the account, she can do those things! If not, she just waits until the next automatic transfer is complete. Many autistic folks let these accounts build up in value over time before going on a spending binge. There’s nothing wrong with that because it’s a no guilt account!

3. Matching your money to your goals (making the budget)

Remember our common money goals:

☐Be able to pay for all normal, recurring expenses

☐Be able to pay for normal big expenses

☐Be able to pay for surprise expenses

☐Have savings for when you can’t or don’t work

☐Use less than you earn

☐Use more than one kind of savings

Once we get a grasp on how we currently spend money, we can make informed decisions about what we can change:

Sarah spends $1411.67 on regular, recurring expenses.

She also spends about $500 in necessary variable expenses.

Together, this $1911.67 is well under her $2500 monthly income. This satisfies these goals:

☐Be able to pay for all normal, recurring expenses, and

☐Use less than you earn

Now let’s help Sarah prepare for normal and unexpected expenses, times when she might not work, and save for the future.

Sarah heard that she should save 3 to 6 months of expenses for emergencies. But no one told her why or how to save or what constituted an emergency. Let’s change that advice to something more practical.

Sarah will use savings for these situations:

To purchase or make a down payment on something big (like a vehicle or house)

To pay for large, necessary, unplanned expenses that cannot come from the variable expense account,

To make ends meet if she loses or leaves a job

Which takes care of these goals:

☐Be able to pay for normal big expenses

☐Be able to pay for surprise expenses

☐Have savings for when you can’t or don’t work

Sarah will build her savings three ways:

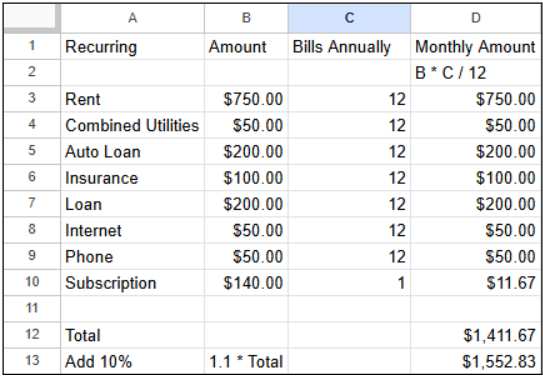

Over-contribute to recurring expenses. (I will show you how in just a moment.)

Add money to a savings account as a regular expense.

(We will discuss this more in Part 3)Increase regular contributions to an investment account.

(We will discuss this more in Part 4)

Sarah will over-contribute to her recurring expenses budget by 10%. If she doesn’t spend it, in less than a year she will have a full month’s worth of expenses saved in her primary account. If she got paid biweekly, then months with an extra paycheck will build this even faster! The extra money in her primary account becomes security against unemployment, job transitions, and lifestyle creep. In less than a year, she could leave her job for a better one without worrying about how to pay bills during the gap between paychecks!

4. Spend according to plan

Let’s look at how Sarah implements her budget.

She set up her accounts at Ally, which allows direct deposits and automatic transfers. She closed her account at a big bank that charged her a monthly fee and moved all her recurring expenses to the primary account. She only uses the debit card for that account when setting up automatic payments online and keeps it somewhere safe.

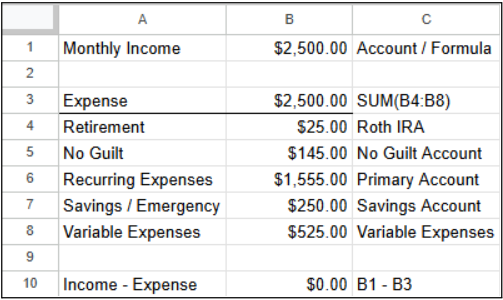

On the 28th of each month, her primary account automatically transfers $250 to her savings account, $525 to her variable expenses account, $145 to her no guilt account, and $25 to a Roth IRA. This helps her feel like each month starts new.

Sarah treats her variable expense account as if she’s running a business. She knows what goes on that debit card - and nothing else!

She now has no problem getting her nails done every few weeks, and enjoys a weekly coffee out with friends, too. She checks her account from her phone before she goes shopping.

She also knows that she might need to rebalance after a month or two. That’s okay, because she’s meeting her goals!

“Getting started is more important than becoming an expert.”

In our next post, we’ll discuss how she’s maximizing her savings account.

Do you have a budget? How do you make your finances manageable?